In its recent Financial Stability Review (FSR) report, the Macroprudential Surveillance Department of the Monetary Authority of Singapore (MAS) assessed the extent to which FinTech companies could disintermediate Asian banks and erode their operating income over the next five years. MAS’ analysis finds that the FinTech challenge is generally more significant in the payments than in the deposit and lending business. This is especially so for banks in Hong Kong, Korea and Singapore, in view of their greater reliance on payment fee income.

The report notes that FinTech presents opportunities for banks to improve their profitability from both the cost and revenue angles, whether exploited either internally within banks or through collaborative partnerships with FinTech companies.

Analysis from McKinsey is quoted, saying that cost savings from leveraging on FinTech, for instance via automation of banking functions or the use of artificial intelligence, could yield a 30% reduction in costs, representing 10% to 20% of Asian banks’ operating income.

FinTech can also facilitates potential revenue growth for banks, for instance through reaching out to new customers via mobile services, especially in countries with relatively lower financial inclusion. The report cites the example of DBS Digibank in India and Indonesia. The move towards cashless payments could also benefit banks, if such digital payment platforms are linked to bank-issued cards.

Increased revenues from innovative new offers and business models could increase banks’ net profits by 5%. Furthermore, new products, distinctive digital sales and using data to cross-sell products could increase banks’ net profits by a further 10%.

FinTech companies are beginning to offer services that disintermediate banking services. The competitive threat and its corresponding impact is expected to vary across business lines. Analysts have highlighted that there is relatively more FinTech investment in retail and consumer banking, especially in the areas of deposit-taking, lending and payments. This view was corroborated by MAS’ discussions with banks that operate in Asia. The MAS study therefore focuses on the impact of FinTech on banks’ operating income in these areas.

Potential reduction in fee income and net interest income

The study estimated the potential reduction in banks’ payment fee income and net interest income owing to disintermediation by FinTech companies. The analysis is based on a downside scenario where banks fail to take mitigating actions to address the competition.

Fee income

Firstly, FinTech companies could offer payment options that compete directly with debit and credit cards issued by banks. This may erode banks’ fee income through lower payment transaction volumes as consumers switch

to FinTech payment channels; and lower fees as banks reduce the Merchant Discount Rate (MDR) that they charge for card payments in response to more competitive transaction fees offered by FinTech companies.

Using third-party information, MAS assessed the probability of payments disintermediation based on: 1) Pre-existing scale of FinTech adoption; 2) Conduciveness for FinTech to develop in terms of the regulatory environment, extent of government support and proximity to relevant expertise; 3) Customer readiness, based on forecasted internet and mobile penetration rates in five years.

Based on these factors, each economy is assigned a rating based on a scale of 1–5, with 1 and 5 representing a low and high probability respectively of payments disintermediation within the next five years. Each rating is then mapped to a projected FinTech payments adoption rate, expressed as a proportion of Household Consumption Expenditure (HCE).

MAS summed up the reduction in operating income from both lower payment transaction volume and margin erosion. The report cautions that the estimated losses would probably be overstated as there would likely be some offsetting effects.

Net interest income

MAS also considered the impact of FinTech on net interest income from deposit and lending business. FinTech enables pure play digital banks to be set up at lower cost than traditional banks, which could enable these new players to offer more attractive deposit rates. This poses a threat to incumbent banks by eroding their deposit funding base and increasing banks’ funding costs as they would need to either raise deposit rates to retain deposits or seek more costly funding in the interbank market. This would erode banks’ interest margins.

Alternatively, banks may reduce lending volumes if they are unable to secure adequate funding. Either strategy would result in lower net interest income.

MAS estimated the potential loss of deposit funding using third-party information on the share of the banked population that is prepared to switch to pure play digital banks and the proportion of deposits that they would be willing to move to such banks. MAS then derived the potential increase in funding costs (and the resulting fall in net interest income) if the banks try to fill the funding gap by borrowing from the interbank market or by raising deposit rates to the interbank rate.

Alternatively, assuming that banks choose to reduce lending to maintain their Loan-to-Deposit (LTD) ratios, MAS estimated the drop in net interest income as a result of lower business activity.

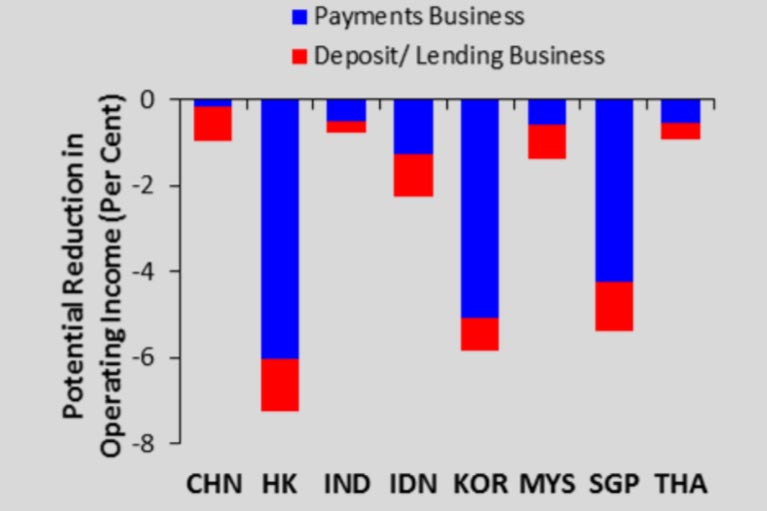

The chart below from the report illustrates the impact of disintermediation on banks’ net interest income. MAS assumed that banks would take the option that would lead to a smaller drop in operating income. For example, banks in Singapore would likely increase their deposit rates and/ or seek interbank funding as opposed to reducing their loan volumes.

The chart at the top of the article aggregates the estimated impact of FinTech-driven disintermediation on banks’ payments, deposit-taking and lending businesses. With the exception of Chinese banks, banks in Asia would generally face larger potential reductions in operating income from their payments business, relative to their deposit and lending business.

This is especially so for banks in developed Asia due to their greater reliance on payment fee income. As mentioned earlier, the report says that estimated potential reduction in operating income is based on an unmitigated scenario in which banks do not take actions to address the FinTech competition. Banks that harness technology could perform better compared to those that do not. The pace of a bank’s digitalisation would depend on factors such as its ability, such as its resources, knowledge, and availability of talent) and openness to adopting technology.

The impact of FinTech on banks could be further differentiated depending on other bank-specific factors. For example, larger banks have broader customer bases that could make them more attractive to talent or to FinTech companies for partnership opportunities. However, the report also cautions that larger banks could be bogged down with large legacy systems, making them less nimble in their digitalisation journey.

As more data becomes available, the study could be expanded to include other business lines, such as wealth management, insurance and remittance. The analysis can also be extended to assess potential second-round effects from FinTech disruption. For instance, disintermediation would reduce transaction flows and the amount of customer data that banks could collect about their clients. With fewer insights on their customers, banks would have fewer cross-selling opportunities and their risk assessments may become less robust.