The World Economic Forum (WEF) released

its first ‘Readiness for

the Future of Production Report’, (“the Report”) assessing how well-positioned global economies

are to shape and benefit from changes in production being driven by the Fourth

Industrial Revolution. The report was developed in collaboration with A.T.

Kearney.

Singapore is among the 25 countries assessed to be in the

best position to benefit from the changing nature of production.

Assessment framework

The Report uses a new benchmarking framework, diagnostic

tool and data set to help countries understand their current level of readiness

for the future of production, as well as corresponding opportunities and

challenges.

The assessment framework is made up of two main components: Structure of Production, or a country’s

current baseline of production, and Drivers

of Production, or the key enablers that position a country to capitalize on

the Fourth Industrial Revolution to transform production systems. There are 59

indicators across these two components.

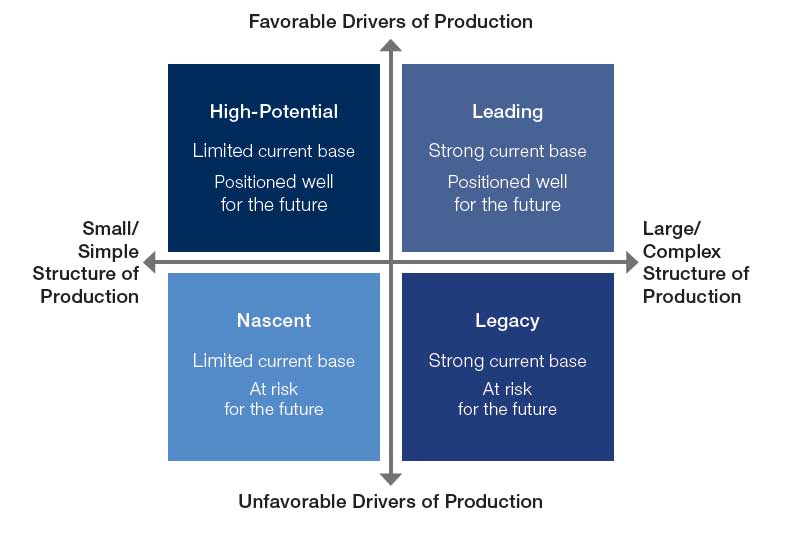

The 100 countries and economies included in the assessment

are assigned to one of four archetypes based on their performance in the

Drivers of Production (vertical axis) and Structure of Production (horizontal

axis).

The assessment measures readiness for the future, rather

than performance today. It assesses the entire country on average, not just the

highest-performing areas within a country. It does not look at sub-regional

differentiation within a country.

The report finds that global transformation of production

systems will be a challenge, and the future of production could become

increasingly polarised in a two-speed world. Of the 100 countries and economies

included in the assessment, only 25 countries from Europe, North America and

East Asia are Leading countries, or in the best position to benefit from the

changing nature of production. These 25 countries already account for over 75% of

global Manufacturing Value Added (MVA) and are well positioned to increase

their share in the future.

The 25 Leading countries in alphabetical order are: Austria, Belgium, Canada, China, Czech Republic, Denmark, Estonia, Finland, France, Germany, Ireland, Israel, Italy, Japan, Republic of Korea, Malaysia, Netherlands, Poland, Singapore, Slovenia, Spain, Sweden, Switzerland, United Kingdom and United States.

The rest of the 100 includes 10 Legacy countries, 7 High-Potential countries/economies and 58 Nascent countries.(Complete rankings can be found in Table3.1 on page 12 of the Report.

Singapore's position

Singapore is among the above mentioned 25 Leading countries.

It ranked 11th for the Structure of Production, and 2nd for Drivers

of Production. It ranks in the top 20 for economic complexity and performs well

across all Drivers of Production, except Sustainable Resources. Within the

Sustainable Resources driver, Singapore contributes less emissions than other

Leading countries, but has challenges related to baseline water stress and

alternative energy sources.

The assessment finds Singapore to be a leader on the Global

Trade & Investment driver as one of the most open and trade-friendly

countries in the world. The Report highlights Singapore’s strong Institutional

Framework and future-oriented approach (the recent

launch of the Singapore Smart Industry Readiness Index is mentioned as an

example) of the Government as key strengths.

Mr. Lim Kok Kiang, Assistant Managing Director, EDB , commented on the report, "Singapore’s strong performance in the Drivers of Production reflects

our commitment and early efforts in building an ecosystem to drive the adoption

of advanced manufacturing amongst our MNCs and SMEs. The launch of the Singapore

Smart Industry Readiness Index, a world-first tool to help industrial companies

harness the potential of Industry 4.0, and Hannover Messe staging its first

Asia edition in Singapore later this year, will reinforce our efforts.

Transformation is a multi-year journey, and more needs to be done. It is

important that we continue working closely with companies, trade associations

and unions to improve our competitiveness and ensure our workforce is well

equipped to support and enable the future of production."

Key general findings

The findings are intended to catalyse multi-stakeholder

dialogue to inform the development of modern industrial strategies. The report

recommends leaders from both the public and private sectors to work together to

address key challenges, build on opportunities and define joint actions at the

national, regional and global level.

The Report finds that the Fourth Industrial Revolution will

trigger selective reshoring, nearshoring and other structural changes to global

value chains. Emerging technologies will change the cost-benefit equation for

shifting production activities and, ultimately, impact location attractiveness.

All countries must develop unique capabilities to make them attractive

production destinations and capitalise on these shifts.

Another key finding of the report is that different pathways

will emerge as countries navigate the transformation of production systems. Not

all countries may seek to pursue advanced manufacturing in the future.

Some

countries that are next in line as the low-cost labour destinations may still

seek to capture traditional manufacturing opportunities in the near term (the

benefits of low-cost labour will be altered by the emerging technologies, as

was also highlighted in a recent

World Bank report). Others will pursue a dual approach, or prioritise other

sectors altogether.

The report also says that all countries have room for

improvement. Though there are early leaders, no country has achieved full

readiness, let alone harnessed the full potential of the Fourth Industrial

Revolution in production.

The assessment also finds common challenges within each

archetype (as seen in chart above: Leading, Legacy, High Potential and Nascent)

and countries can learn from each other, while pursuing their own unique

strategy.

Leading countries need to convert readiness into actual

transformation and push the frontier by designing, testing and pioneering

emerging technologies. Legacy countries need to avoid getting squeezed between

more advanced Leading countries, which can offer more advanced manufacturing,

and Nascent countries that can offer lower cost labour. High-Potential

countries and economies have capabilities that can potentially be converted to

strengthen their Structure of Production and further diversify their economy. Their

key challenge is expected to be to find the right balance across sectors when

determining economic priorities. For nascent countries, the challenge will be

to determine whether to pursue advanced manufacturing or traditional

manufacturing, and to what extent.

The report also notes that though technological advancement

brings the potential for leapfrogging, but only a handful of countries are

positioned to capitalise. Lagging countries could enter emerging industries at

a later stage without the legacy costs of earlier investment, but only if they

have the right set of capabilities and develop effective strategies.

However, readiness for the future of production requires

global, not just national, solutions. Globally connected production systems

need not only sophisticated technology but also standards, norms and

regulations that cross technical, geographical and political boundaries. This

would be necessary to release efficiencies and make it easier to do business

across global value chains.

Moreover, the report recommends that new and innovative

approaches be explored for public-private collaboration to accelerate

transformation. Every country faces challenges that cannot be solved by the

private sector or public sector alone.

New approaches to public-private collaboration that

complement traditional models can help governments quickly and effectively form

partnerships that unlock new value.

It is also important to note that the assessment framework

is based on two key hypotheses and working assumptions that will be tested and

researched over time.

The first is that the most important drivers of future

readiness are Technology & Innovation, Human Capital, Institutional

Framework and Global Trade & Investment. These drivers have the strongest

correlation with economic complexity. The needs within each driver are expected

to evolve, but the overall drivers will remain significant.

The second is that scale is not a prerequisite for future

readiness.

Economic complexity is more important than scale for readiness for

the future of production. The ability to gather, combine and use knowledge

embedded in people and technology to create a range of unique products will

become an increasingly important competitive advantage. Thus, small countries

such as Switzerland or Singapore are not necessarily at a disadvantage against

global giants with larger scale.

Read the complete report here.