1. Restricted Community Mobility (Best chance to beat COVID-19)

Keeping people at home is noticeably slowing the spread of the virus. The rates of infection in locked-down areas have slowed albeit not as quickly as desired in some places.

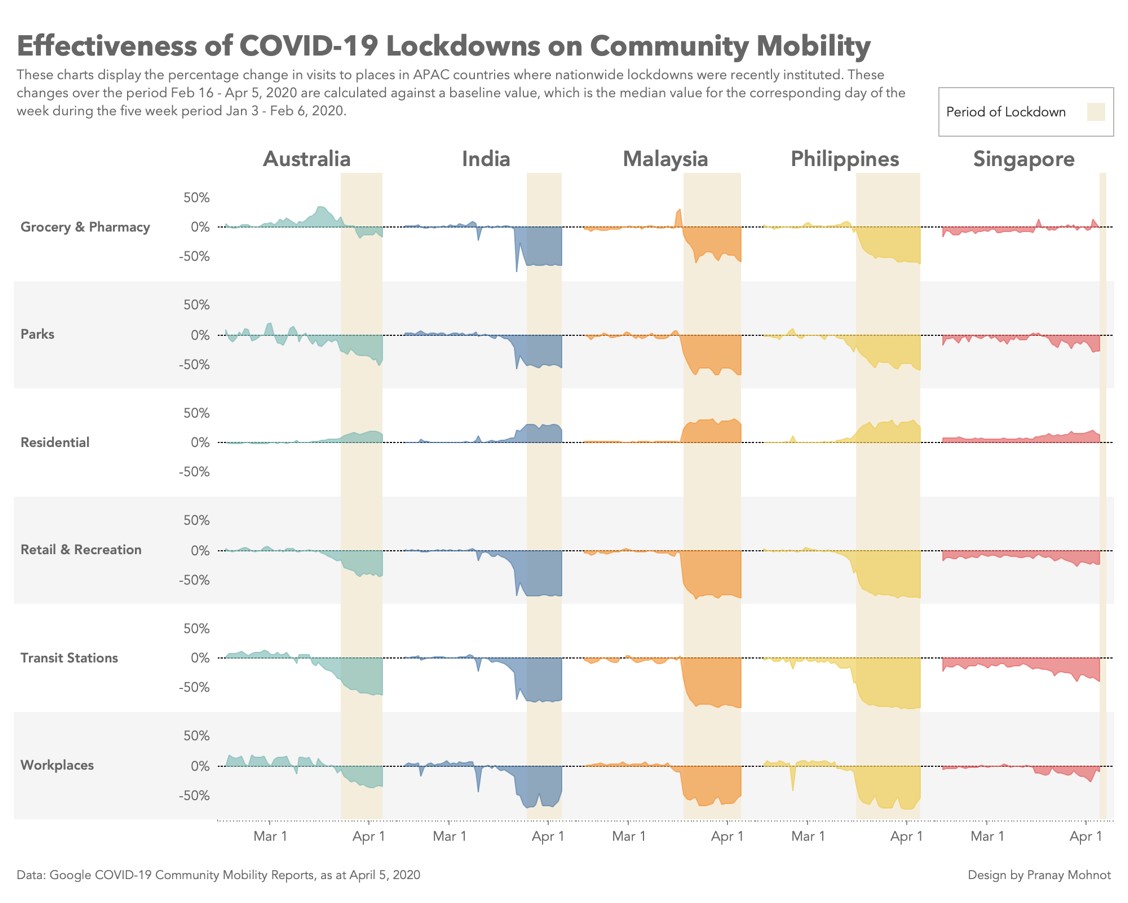

To help public health officials better understand the movement of people, Silicon Valley giants Apple and Google have begun releasing reports documenting relative changes in community mobility. These reports use anonymous locational data from their maps services to track daily changes in the movement of users against a baseline value.

Specifically, Google is using the average number of visits to places for each day of the week over a five-week period in January as its baseline. Crucially, visits to these places are aggregated by the type of establishment.

These tags present a key aspect of the dataset as they allow users to identify mobility trends by the category that a place belongs to. The data shows percentage deviations from the baseline in January, back when things were largely normal.

Things are hardly normal now. In almost every society, schools and workplaces are shut, while only essential services are allowed to carry on.

The World Economic Forum reported that nearly 3 billion people—close to half of the world’s population—have come under COVID-19 lockdowns. This number is likely higher now as the outbreak worsens and governments take even more stringent measures.

The dust appears to be settling in Western Europe however which was one of the first few regions outside China to be impacted by the virus.

As Spain and neighbouring countries begin to ease their lockdowns, it is worthwhile to take stock of the effectiveness of their safe distancing measures. A second wave of infections is upon us, as evidenced by ongoing events in Beijing.

In the above visualisation, it is not surprising that visits to grocery shops and pharmacies peaked before lockdowns came into effect, probably due to bouts of panic buying.

Potential uses of this data could include restocking supermarkets in advance to cope with a surge in demand or developing internet infrastructure to cope with higher demand from residential areas.

The right use of actionable data will help policymakers gauge the efficacy of their regulations. It can aid in the enforcement of lockdowns, as well as enable a targeted and phased reopening of the economy.

Both Apple and Google should be commended for their efforts in making anonymised data transparent and available for policymakers to gain valuable insights. We hope to see more such public interest initiatives in the future.

2. Costly Miss Explosion of cases in New York

If the state of New York were a country, it would have more COVID-19 cases (as at Mar 29, 2020) than any country other than the US. Such is the scale of the coronavirus situation in New York. T

he state has become the epicentre of the pandemic in America. Notably, the crisis and the ensuing lockdown caused a tussle between New York Governor Andrew Cuomo and US President Donald Trump.

Trump asserted that he has the ultimate authority to reopen the economy and Cuomo has refuted this claim.

Speaking in a CNN interview, he said, “If he ordered me to reopen in a way that would endanger the public health of the people of my state, I wouldn’t do it.”, referring to Trump.

The governor is looking for a phased reopening which may take months to complete.

The lighter colours in the visualisation above show forecasts that were made in mid-April using data available then. Unfortunately, New York’s recovery has not been as smooth as predicted here. A fresh spike of cases on April 25 has cast uncertainty on its future. This proves the difficulty of predicting the number of cases by fitting a simple model due to the numerous complexities involved in the spread of viruses.

Analysing the timeline of cases, as we go from each day to the next, the number of infections is multiplied by some constant. The spread of viruses is a textbook example of exponential growth because what causes the new cases are the existing ones. This is why we have put the y-axis on a logarithmic scale—each step of a fixed distance corresponds to multiplying by a certain factor. On this scale, exponential growth should look like a straight line. This straight line does not go on forever. It has to start slowing down at some point. The key question is when.

Owing to rigorous social distancing, it looks like New York has passed the peak, and the line of cumulative cases is slowly flattening. Now, governments worldwide are mulling over when to reopen their economy. Too early, and we could see another spike in infections. Too late, and the impact on the economy may be irreparable.

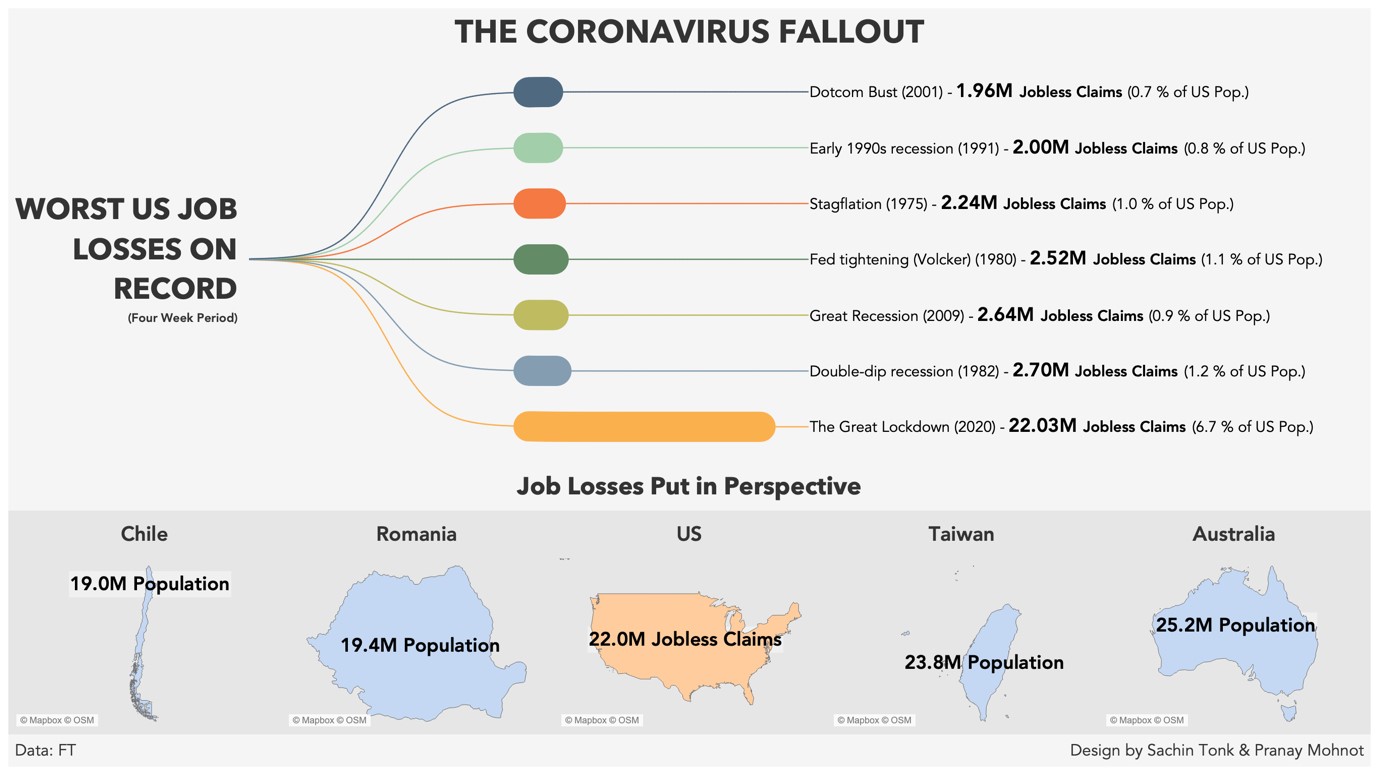

3. No Job – The New Normal

The impact of the pandemic on employment in unmistakable. As with recessions of the past, job losses were expected. What differentiates this downturn from any other is the enormity of these job losses. Instead of a gradual decline in economic activity as seen in business cycle depressions, business operations have ground to a halt, creating shockwaves in the national and global economy.

The current economic situation has been dubbed The Great Lockdown. A shutdown so fast and job losses so many have never been experienced before.

The above visualisation looks at the worst US job losses on record. These are measured over a four-week period. To account for population growth, the number of jobless claims as a percentage of the US population is also shown.

In case the true scale of this crisis not been emphasised enough, the number of job losses is about ten times higher than the average number of job losses in recessions since 1975. The number stands at a staggering 22.03 million, which is almost equal to the populations of middle powers such as Taiwan and Australia.

The recovery of jobs from the last recession was very slow. It took roughly ten years for the US economy to return to an unemployment rate similar to pre-recession levels.

Like other recessions, The Great Recession took many months to culminate. The current crisis is different in that businesses have been suddenly forced to pause operations. One can hope that businesses are able to stay afloat during this shutdown and rehire workers once normalcy resumes.

Besides temporary shocks, the pandemic will result in structural changes in the global economy. In the microeconomic context, it will expedite the adoption of technologies like e-learning and e-commerce.

Telecommuting will be normalised, and more firms will provide the option to work from home. Politically, this pandemic will test the effectiveness of various institutions and it could determine upcoming elections.

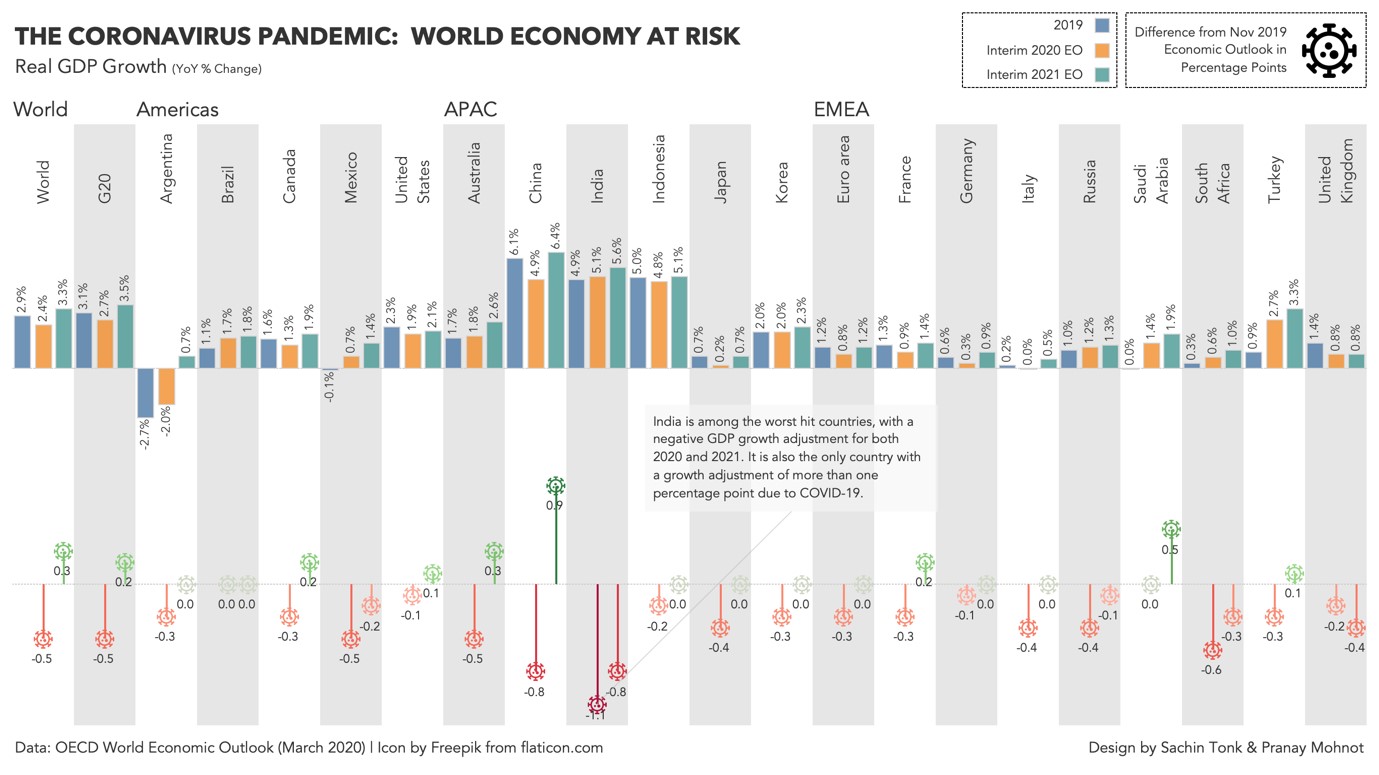

4. World Economy at Risk

The Organisation for Economic Co-operation and Development (OECD) published an interim economic assessment in March 2020.

Importantly, it has revised its growth projections from November last year. In most countries, the growth adjustment is negative for 2020 but positive for 2021.

Mature economies like the US will take a slight hit in 2020 but will recoup their losses in the following year. Emerging economies on the other hand like India will be badly hit economically.

India has negative GDP revisions in both 2020 and 2021 and, as such, its recovery is likely to be slow. China, being the earliest to recover from the pandemic, will have the greatest jump in growth in 2021 at 0.9 percentage points.

Argentina’s economy was already shrinking and shocks from this pandemic will not do it any good. It is clear from this economic outlook that the timing of economic effects will vary across countries.

The GDP growth forecasts have been adjusted because the world economy is being buffeted by both demand and supply-side shocks.

Authors Philipp Carlsson-Szlezak, Martin Reeves and Paul Swartz (2020) summarised three main shocks in an article for Harvard Business Review (HBR).

The first demand shock is an indirect hit to consumer confidence. Turmoil in financial markets has lowered household wealth.

Macroeconomics fundamentals tell us that this must result in higher household savings and less consumption. Advanced economies are more predisposed to this as their household exposure to the equity asset class is high.

Secondly, there will be a direct hit to consumer confidence. As consumers are forced to isolate themselves, they may reduce their discretionary spending and be less optimistic about the future.

Lastly, a supply-side shock results as the pandemic causes production to cease and disrupts key components of supply chains. This would lead to greater unemployment, but the effects would differ across industries. The crisis may not last long enough for this shock to be significant.

While the above data is useful, the authors of the HBR article warn against becoming too dependent on projections. Instead, leaders should look past the crisis, scanning for opportunities and challenges, and considering how they would address the post-crisis world.

Reference

What coronavirus could mean for the global economy. (2020, March 3). Harvard Business Review. Retrieved from https://hbr.org/2020/03/what-coronavirus-could-mean-for-the-global-economy